FEMA's New Hospital DOB Decisions Are a Warning for Pending COVID-19 PA Claims

After a lengthy silence on the subject and leaving numerous first and second appeals waiting beyond the statutory response time, FEMA recently issued a cluster of second appeal decisions denying or reducing otherwise eligible Public Assistance (PA) funding for COVID-19 medical-care claims based on duplication of benefits (DOB). These recently issued decisions demonstrate that FEMA is doubling down on its Standard Method Review for determining duplication between claimed costs and patient care revenue. Applicants must work even harder to meet the burden and convince FEMA that there is no prohibited DOB. With the eligibility bar clearly raised and FEMA tightening its reviews, applicants with pending appeals should consider all options, including whether continuing to pursue funding through the arbitration process available for large claims could provide a more equitable path for review and possible success.

How the Standard Method Works

FEMA's review is not limited to whether a particular diagnostic test, labor hour, or supply item was separately billed and paid for by a patient and/or the patient's insurance. FEMA's Standard Method Review uses a broader ceiling-based analysis that compares patient care revenue and operating expenses to determine how much FEMA can reimburse in a cost category and calendar year without duplicating another source of funding.

First, FEMA sorts claimed costs into Labor, Supplies and Services, and Equipment cost categories. It then assesses whether the claimed costs have a low or high likelihood of being duplicated by patient care revenue. Costs with a low likelihood of duplication, such as personal protective equipment, are not charged to patients and generally are not limited by patient care revenue ceilings. Costs with a high likelihood of duplication with patient care revenue, such as COVID-19 tests and labor to treat COVID-19 patients, are subject to potential reduction under the Standard Method Review.

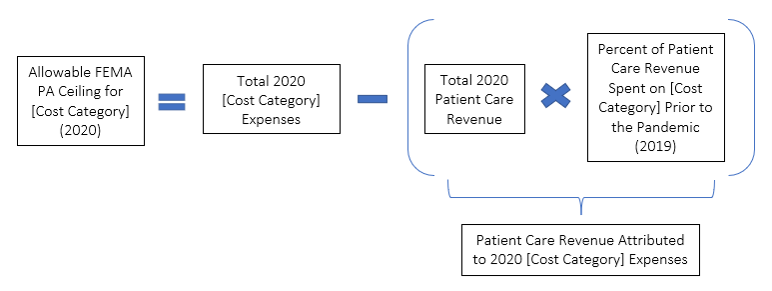

Next, FEMA calculates the Allowable Ceiling, the amount that FEMA may fund in a certain cost category per year without duplicating benefits. To calculate the Allowable Ceiling, the Standard Method generally includes review of the applicant's financial data for the one-year period immediately prior to the COVID-19 pandemic to evaluate the proportionate amount of patient care revenue assumed available to cover each cost category. These benchmarks are then applied to revenue and costs for the pandemic years 2020 – 2023 to produce resulting presumptions of the amount of patient care revenue available to cover costs and, correspondingly, the "Allowable Ceiling" amounts left over that FEMA may fund without the applicant incurring a duplication of benefits.

Below is an example of how the Allowable Ceiling is calculated using the Standard Method. The same equation is used to calculate Allowable Ceilings for all cost categories across each of the pandemic years.

Finally, high-likelihood costs debit the Allowable Ceiling for the corresponding year and cost category. Costs within the ceiling should not be reduced for patient care revenue DOB. High-likelihood costs above the ceiling, or in a zero- or negative-ceiling cost category year, are treated as duplicative, and FEMA will reduce the corresponding amount from the applicant's otherwise eligible claims.

FEMA applies ceilings across all of the applicant's COVID-19 projects. Multiple projects therefore compete for the same bucket, and once it is exhausted, reductions are applied chronologically based on project creation date in Grants Portal.

That is why claiming that a cost was not separately billed to a patient, and therefore cannot be tied to patient care revenue, will not be enough to confer eligibility. FEMA looks at the aggregate Allowable Ceiling for each year per and cost category, not at whether the individual cost was billed to a patient and subsequently paid.

Why Cost Classification and Timing Matter

Under the Standard Method, proper classification of costs under the Standard Method Review process is a practical pressure point. Costs entered in Grants Portal under PA categories such as Labor, Contract, Material, Equipment, and Rental Equipment must be reclassified under FEMA's Standard Method ceiling categories: Labor, Supplies and Services, and Equipment.

That remapping of costs can change the result because FEMA calculates a separate ceiling for each category in each calendar year. Moving costs between categories can preserve or consume available ceiling. Furthermore, applicants must verify whether a particular cost is considered to have a high likelihood of duplication with patient care revenue. Costs classified as having a low likelihood of duplication should not be at risk of reduction regardless of the corresponding Allowable Ceiling.

Timing can have the same effect. FEMA calculates ceilings by calendar year and, for multiyear projects, apportions costs by year based on project documentation when feasible. If timing is unclear, FEMA may assume equal monthly spending, potentially shifting costs into a year with less available ceiling than expected. For example, assume a hospital has remaining 2021 Supplies and Services ceiling but has exhausted its 2021 Labor ceiling. If a mixed contract invoice is not broken out and FEMA classifies the entire amount as Labor, DOB exposure may increase. If the hospital documents that part of the invoice reflects eligible Supplies or Services, that portion may be assigned to a category-year with available ceiling.

Applicants should build the DOB crosswalk before FEMA does it: map general ledger entries, FEMA PA cost codes, invoices, and work dates to Standard Method category-year buckets; identify high- and low-likelihood costs; and explain allocation assumptions in the claim record. This can help preserve Allowable Ceilings and avoid preventable reductions.

What FEMA Seems to Be Consistently Rejecting

The recent decisions show FEMA repeatedly rejecting arguments that do not engage with the mechanics of the Standard Method Review. FEMA's legal premise is that Stafford Act § 312 prohibits FEMA from duplicating assistance an applicant receives from any other program, insurance, or other source, and FEMA places the burden on the applicant to provide documentation and explain how its records support the appeal.

FEMA repeatedly rejected broad statements that claimed costs were not covered by other sources when the applicant did not provide a documented analysis reconciling those assertions with patient care revenue, insurance, and the Standard Method's Allowable Ceilings. FEMA has rejected the following arguments in its recent second appeal decisions:

- Item-level billing arguments: In denying a second appeal filed by King's Daughters Medical Center (Mississippi), FEMA rejected the argument that the claimed tests were not directly billed to patients or were associated with billing codes that were not ultimately used. FEMA instead relied on its broader view that hospitals generally do not link patient care revenue to specific expenses on a patient-by-patient basis.

- Fiscal-year alternate methodologies: In multiple Pennsylvania hospital appeal denials, including those for Ephrata Community Hospital, Inc. (Lancaster County) and The Good Samaritan Hospital of Lebanon (Lebanon County), FEMA rejected alternate methodologies based on fiscal-year data where applicants did not show that the fiscal-year approach was more accurate than FEMA's calendar-year Standard Method Review.

- Accounting-practice explanations: In addition to the above, FEMA also rejected arguments by Waynesboro Hospital (Franklin County, Pennsylvania) that fiscal years should control simply because hospital reports, audits, and internal processes are organized that way; FEMA focused instead on whether the method captured the relevant pre-pandemic and pandemic comparison needed for the DOB analysis.

- Spreadsheets without an explanatory bridge: In its denial for Gettysburg Hospital Corporation (Adams County, Pennsylvania), FEMA refused to accept revenue and expense spreadsheets as sufficient unless the applicant also explained how the documents showed that the Standard Method Review was inaccurate or that the proposed Alternate Method Review was more accurate.

What Hospital Systems Should Do Now

Not all hope is lost if your organization has received a COVID-19 DOB reduction. For example, our team has seen success at the First Appeal level by demonstrating to FEMA that the presented alternative analysis is more accurate than FEMA's Standard Method Review. Similarly, we have been successful working with FEMA to demonstrate that an applicant's alternate methodology is more reliable than the Standard Method prior to issuance of a Determination Memorandum.

Hospitals with pending claims should treat the Standard Method Review as the starting point for claim strategy. That means building a project-specific DOB narrative that reconciles claimed costs against patient care revenue, insurance, federal relief funding, state assistance, and any other reimbursement sources while explaining how the hospital's records interact with FEMA's Allowable Ceiling analysis.

- Build the DOB record early. Assemble revenue, expense, insurance, and other assistance documentation before FEMA issues a determination.

- Do not rely on accounting preference alone. If using fiscal-year or other alternate data, explain why that method is more accurate for DOB purposes.

- Connect the numbers to the legal standard. A spreadsheet should be accompanied by a narrative that walks FEMA through the non-duplication analysis.

- Address FEMA's assumptions directly. Explain where the Standard Method Review overstates duplication and support that explanation with contemporaneous records.

- Review all claims for any prior reductions and ensure all costs are properly included in any analyses and any previously submitted but rejected reductions are reconciled as part of the final review.

Baker Donelson's Disaster Recovery and Government Services Team is one of the only groups in the nation dedicated to this area of law, with experience involving billions of dollars in disaster assistance from FEMA, HUD, and other agencies working for clients in more than 40 states and territories across approximately 30 federal grant programs.

For health systems, that experience translates into practical support at each stage of the FEMA Public Assistance lifecycle: pressure-testing claims before submission, building DOB and source-of-funding analyses, organizing the documentation FEMA expects to see, responding to requests for information, challenging adverse determinations, and navigating FEMA's appeal and arbitration processes when needed.

The team's multidisciplinary perspective is particularly valuable in hospital DOB disputes because these matters require more than legal argument. They require a coordinated understanding of FEMA policy, grant compliance, health care revenue streams, insurance and other assistance, financial documentation, and how to present a defensible administrative record.

For questions about FEMA's Standard Method Review or about any other aspect of FEMA's DOB process or claims generally, please contact Wendy Huff Ellard, Chris Bomhoff, or any member of our Government Solutions and Public Funding Group.